The Anatomy of a Liquidity Event: Deconstructing the Post-Holiday Market Fracture

The resumption of trading on the Indonesia Stock Exchange (IDX) on Tuesday, April 8, 2025, following the extended Idul Fitri holiday suspension, precipitated a severe liquidity event characterized by a rapid, non-linear repricing of geopolitical risk premiums that fundamentally altered the short-term valuation landscape of Indonesian equities. The Jakarta Composite Index ($IHSG) experienced a precipitous decline, triggering a trading halt after breaching the 8% downside threshold at 09:00 AM WIB, eventually closing the session with a massive contraction of 7.71% to settle at 6,008.4.

Line chart of Jakarta Composite Index (IHSG) with timeframe 3 Months.

This correction, while optically severe and statistically anomalous relative to typical daily volatility bands, represents a delayed synchronization with global markets that had already begun discounting the deleterious implications of the United States Administration’s announcement regarding a proposed 32% reciprocal tariff on Indonesian imports. The market behavior observed on April 8 is not merely a reaction to trade policy mechanics but reflects a broader, structural capitulation of foreign institutional capital, which utilized the high liquidity of large-cap banking constituents to exit positions into a domestic liquidity vacuum created by the extended holiday absence. The magnitude of the sell-off, which saw the erasure of significant market capitalization in a single session, was exacerbated by the structural changes in the IDX trading mechanisms, specifically the harmonization of the Auto Rejection Bottom (ARB) limits to a symmetrical 15%, a policy shift that acted as a liquidity accelerant in a panic-selling environment.

The convergence of three distinct drivers—the geopolitical shock of the Trump tariff announcement, the structural fragility introduced by the new ARB rules, and the cyclical liquidity drought typical of the post-Lebaran period—created a perfect storm for asset mispricing. The Jakarta Composite Index’s plunge to the 6,008.4 level implies a market pricing in a worst-case scenario of immediate, full implementation of punitive tariffs, ignoring the nuances of diplomatic negotiation and the historical precedent of transactional trade diplomacy. However, for domestic institutional investors and sophisticated private capital, this dislocation presents a distinct structural opportunity, particularly within conglomerate equities where controlling consortiums possess both the balance sheet capacity and the strategic incentive to defend valuation floors.

The divergence between the indiscriminate selling pressure driven by macroeconomic headlines and the idiosyncratic capital management strategies of major Indonesian conglomerates—specifically those with active share repurchase programs and consolidated ownership structures like the Barito Pacific Group—creates a compelling entry point for capital willing to look past the immediate volatility of the tariff shock. The selling pressure on April 8 was notably concentrated in blue-chip banking stocks such as Bank Rakyat Indonesia ($BBRI) and Bank Mandiri ($BMRI), which fell 7.65% and 8.27% respectively, acting as the primary liquidity ATMs for foreign outflows, while the underlying credit fundamentals of these institutions remain robust and largely insulated from direct trade tariff transmission mechanisms.

Comparison chart of BBRI, BMRI with timeframe 6 Months.

It is critical to understand that the April 8 crash was not a reflection of systemic domestic economic failure but rather a liquidity mismatch event where the backlog of negative global sentiment accumulated during the holiday week of March 31 to April 7 was forced through the narrow funnel of the opening auction on April 8. The resulting price action, characterized by a gap-down opening and sustained selling pressure, pushed valuations of key conglomerate assets into deep value territory, well below intrinsic levels implied by their asset bases and contracted revenue streams. For instance, the renewable energy sector, despite having long-term USD-pegged revenue contracts with state utilities that act as a natural hedge against currency depreciation, suffered alongside export-oriented manufacturing sectors, illustrating the indiscriminate nature of the sell-off. This lack of discrimination by the broader market is the precise mechanism that generates alpha for investors aligned with the “consortium put”—the implicit or explicit guarantee provided by controlling shareholders who are actively buying back shares at these depressed levels.

The content provided here is for informational purposes only. It is not advice or recommendation. Please do your own research.

The Geopolitical Catalyst: The Mechanics and Implications of the 32% Reciprocal Tariff

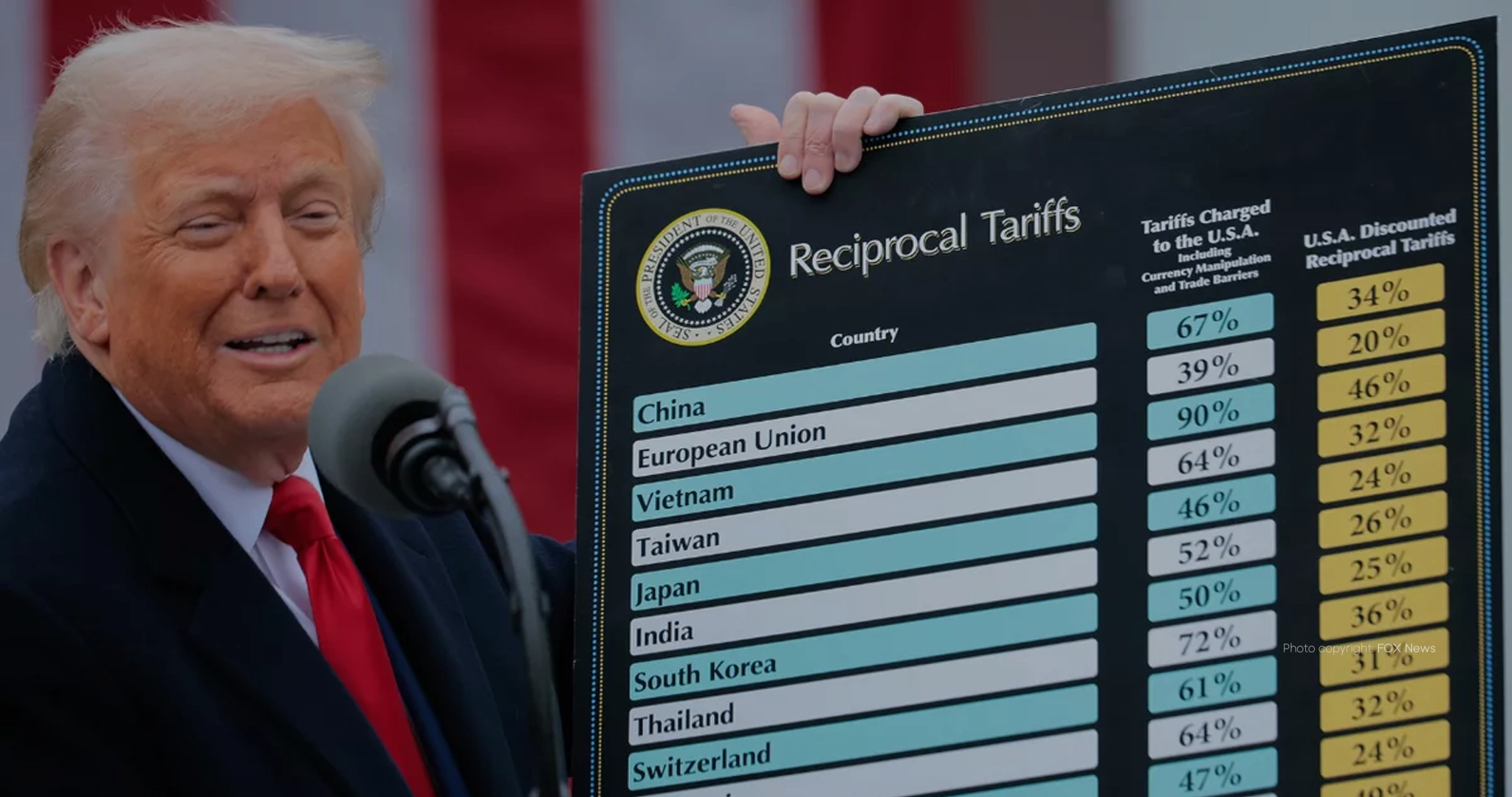

The primary catalyst for the April 8 liquidation event was the formal notification by the United States Trade Representative (USTR), under the direction of President Trump, on April 3, 2025, imposing a 32% tariff on Indonesian goods. This policy action, framed as a “reciprocal” measure to counter perceived trade imbalances and protectionist barriers, struck the market while domestic exchanges were shuttered for the Idul Fitri observance, creating a vacuum of information processing that released explosively upon the market’s reopen. The 32% figure is mathematically derived from the USTR’s calculation of Indonesia’s combined tariff and non-tariff barriers, creating a blunt instrument that affects a broad swathe of the export economy, from textiles and footwear to commodities like rubber and electronics. The USTR’s logic posits that because Indonesia imposes various localization requirements, luxury taxes, and import duties that effectively amount to a 32% barrier for US goods entering Indonesia, the US is justified in levying an equivalent surcharge on Indonesian exports entering the American market.

However, a nuanced analysis of the tariff structure suggests that the market may be over-extrapolating the direct impact on IDX-listed conglomerates, particularly those that do not rely on direct exports to the United States. The transmission mechanism of the tariff shock to the broader economy is secondary; it operates through the channel of Rupiah depreciation (as the trade surplus narrows) and capital flight (as foreign risk appetite wanes) rather than direct revenue erosion for domestic-focused entities. The USD/IDR exchange rate pressure observed on April 8, necessitating intervention by Bank Indonesia in the non-deliverable forwards (NDF) market, confirms that investors are pricing in a deterioration of the current account balance.

Line chart of US Dollar to Indonesian Rupiah (RUPIAH) with timeframe 6 Months.

Yet, for conglomerates with USD-denominated revenue streams or those operating in sectors with high barriers to entry and domestic pricing power, the sell-off represents a mispricing of risk. The diplomatic track, currently being pursued by Coordinating Minister Airlangga Hartarto who was dispatched to Washington D.C., typically yields negotiated settlements involving purchase commitments—such as increased procurement of Boeing aircraft or US agricultural products—rather than the permanent imposition of punitive tariffs.

The announcement of the 32% tariff on April 3, followed by a formal letter from President Trump to President Prabowo Subianto on April 7, solidified the threat just as the market was preparing to reopen. This timing ensured that the negative sentiment was at its peak intensity on the morning of April 8. The market’s reaction reflects a fear that Indonesia’s export competitiveness could be structurally impaired, specifically in labor-intensive industries that operate on thin margins and compete directly with Vietnam and Bangladesh. However, the listed universe on the IDX is dominated by banking, telecommunications, and energy—sectors that are largely insulated from US import tariffs. The banking sector’s decline, for instance, is a function of its high foreign ownership and liquidity, making it the easiest asset class to sell for global funds reducing Indonesia overweight positions, rather than a reflection of deteriorating loan quality due to tariffs. Therefore, the geopolitical risk premium currently priced into the market is likely excessive for the domestic conglomerate sector, creating a disconnect between price and fundamental value that can be exploited by patient capital.

The Role of Regulatory Microstructure: Symmetrical ARB and Trading Halts

The severity of the April 8 plunge cannot be attributed solely to the tariff news; it was significantly amplified by the structural evolution of the IDX’s trading rules, specifically the implementation of symmetrical Auto Rejection limits. During the pandemic era, the IDX utilized an asymmetric Auto Rejection Bottom (ARB) of 7%, which acted as a circuit breaker for individual stocks, limiting the daily downside and preventing panic selling from cascading into deep value destruction in a single session. By April 2025, the IDX had normalized these rules, implementing a symmetrical 15% ARB for the Main Board. This structural adjustment, intended to improve price discovery and liquidity, functioned as a volatility accelerant on April 8. When panic selling commenced at the open, stocks that would have previously locked limit-down at -7% continued to trade lower, seeking liquidity at -10%, -12%, and -14%.

This deeper drawdown capability had a cascading effect on leveraged positions. As stock prices sliced through the previous psychological support levels of -7%, intraday margin calls were triggered for retail and institutional accounts using financing. This forced liquidation created a feedback loop of selling, pushing the index down further and triggering the market-wide trading halt mechanism. At 09:00 AM WIB, the Jakarta Composite Index breached the 5% decline threshold, triggering a 30-minute trading halt designed to allow information dissemination and cool investor sentiment. However, in a high-anxiety environment, the trading halt often has the opposite effect; instead of calming the market, it creates a backlog of sell orders as participants rush to exit before prices fall further. Upon the resumption of trading at 09:30 AM, the selling pressure intensified, pushing the index to its intraday low and resulting in a close of -7.71%.

The implications of the symmetrical 15% ARB are profound for volatility management. It implies that “buying the dip” requires a wider margin of safety and a deeper understanding of order book dynamics. On April 8, stocks like Chandra Asri Pacific and Barito Renewables Energy faced selling pressure that pushed them toward the lower bounds of their trading ranges. However, unlike the broader market which panicked, the specific trading patterns in these conglomerate stocks showed signs of absorption—strategic buying entering the market at deep discounts to soak up the forced selling. This absorption is the hallmark of the “consortium defense,” a mechanism where controlling shareholders utilize the increased volatility to accumulate shares at favorable prices, effectively leveraging the new ARB rules to accelerate their buyback programs.

| Parameter | Metric / Value | Implication for Liquidity Event |

|---|---|---|

| IHSG Closing Level | 6,008.4 (-7.71%) | Deep correction indicating panic capitulation. |

| Trading Halt Trigger | 09:00 AM WIB | Triggered by >5% drop; exacerbated backlog of sell orders. |

| ARB Rule | Symmetrical 15% | Allowed stocks to fall 2x deeper than pandemic-era rules. |

| Tariff Catalyst | 32% “Reciprocal” | Blunt instrument targeting aggregate trade barriers. |

| Foreign Net Sell (Day) | IDR 214.17 Billion | Highly concentrated in Banking/Telco blue chips. |

| Foreign Net Sell (YTD) | IDR 35.86 Trillion | Indicates prolonged structural outflow trend. |

| USD/IDR Impact | High Volatility | Triggered BI intervention in NDF markets. |

The Consortium Defense Thesis: Structural Support in Conglomerate Equities

In the face of such indiscriminate selling, the most resilient segment of the market—and the primary area of opportunity—lies within major conglomerates backed by powerful shareholder consortiums. Unlike standalone companies that are at the mercy of market sentiment, Indonesia’s top conglomerates (such as the Barito Pacific Group, Astra International, and the Salim Group) possess “internal capital markets” and strategic control mechanisms designed to manage equity volatility. The concept of the “Consortium” here refers to the coordinated actions of the controlling families, their private investment vehicles, and allied strategic partners who act to stabilize share prices during periods of extreme dislocation. This support is often manifested through three primary channels: formal share buyback programs, open-market purchases by controlling entities, and corporate actions (such as acquisitions) that signal intrinsic value well above prevailing market prices. On April 8, these mechanisms became the primary line of defense against the tariff-induced rout, effectively creating a “put option” for minority shareholders who align themselves with the controlling interests.

The Barito Pacific Group, controlled by Prajogo Pangestu, serves as the preeminent case study for this defensive capability. In the weeks preceding the crash, specifically on March 21, 2025, PT Barito Renewables Energy Tbk ($BREN) announced a massive share buyback program allocating up to IDR 2 trillion. This corporate action, scheduled to run through June 23, 2025, was explicitly designed to address “significantly fluctuating market conditions”. When the market plunged on April 8, this buyback authorization provided a formidable backstop. While the stock price was inevitably pressured by the broader market beta, the presence of a committed buyer with IDR 2 trillion in firepower effectively sets a valuation floor. Furthermore, the group’s petrochemical arm, Chandra Asri Pacific ($TPIA), has historically engaged in similar stabilization efforts and recently completed value-accretive acquisitions (such as the Aster Chemicals deal) that bolster its asset base. For investors, “buying the dip” in these names is not a bet on market sentiment, but a co-investment with the controlling consortium, which has legally committed capital to defend the stock price.

Sector Analysis: Renewable Energy and The Barito Renewables ($BREN) Opportunity

Barito Renewables Energy ($BREN) represents a unique convergence of defensive characteristics and aggressive capital support. As the largest geothermal operator in Indonesia, BREN’s revenue model is fundamentally decoupled from the US trade tariff risks that precipitated the April 8 crash. Its revenue is derived from long-term Energy Sales Contracts (ESC) with PLN, the state utility, which are typically pegged to the US Dollar or have inflation adjustment mechanisms. This structure provides a natural hedge against the currency volatility triggered by the tariff announcement. Despite this insulation, BREN shares were caught in the broader market liquidation, offering a rare opportunity to acquire a defensive utility asset at a distressed price.

Candlestick chart of Barito Renewables Energy Tbk (BREN) with timeframe 1 Year.

The “Consortium Put” in BREN is explicit. The share buyback program announced on March 21, 2025, authorized the repurchase of up to IDR 2 trillion of shares. This program was active on April 8, meaning that as retail and foreign investors sold into the panic, the company’s treasury was legally authorized and financially capable of absorbing that supply. The rationale for the buyback, as stated in the disclosure, cited “significantly fluctuating market conditions,” a prescient description of the April 8 event. Furthermore, the company’s Q1 2025 financial performance reinforces the disconnect between price and value. BREN reported consolidated revenues of US$150 million, EBITDA of US$130 million (implying an 86.4% EBITDA margin), and Net Profit of US$42 million for the first three months of 2025. These metrics demonstrate operational excellence and high cash flow generation, which supports the company’s ability to fund the buyback without compromising its balance sheet.

The strategic acquisition of the Sidrap wind farm and the ongoing development of geothermal assets at Salak and Wayang Windu provide a clear growth trajectory that is independent of US trade policy. The discrepancy between BREN’s stable, contracted cash flows and the volatile, sentiment-driven price action on April 8 creates a classic arbitrage opportunity. Investors are essentially buying dollars of future cash flow for cents on the dollar, with the downside protected by the IDR 2 trillion buyback wall. The key risk to monitor is the volume of selling relative to the buyback capacity; however, given the low free float of BREN, the buyback funds are likely sufficient to stabilize the price against all but the most catastrophic systemic outflows.

Sector Analysis: Petrochemicals and The Chandra Asri ($TPIA) Transformation

Rp 6,200

MCap: 536.37 T

Chandra Asri Pacific ($TPIA) offers a different but equally compelling narrative of consortium support. Unlike BREN’s utility-like stability, TPIA operates in the cyclical petrochemical industry. However, the company is undergoing a profound transformation into an infrastructure holding company, a shift that was significantly advanced just days before the crash. On April 1, 2025, TPIA completed the acquisition of Aster Chemicals and Energy Pte Ltd from Shell. This transaction is critical for two reasons: first, it diversifies TPIA’s revenue base into midstream energy and infrastructure; second, and more immediately relevant to the April 8 price action, it resulted in a massive “bargain purchase gain” or negative goodwill.

Line chart of Chandra Asri Pacific Tbk (TPIA) with timeframe 1 Year.

In its Q1 2025 financial statement, released shortly after the acquisition, TPIA reported a net income of US$1.6 billion. It is crucial to dissect this figure: the vast majority of this “profit” is accounting-driven, resulting from acquiring Aster at a price significantly below the fair value of its net assets. While this does not represent operating cash flow, it dramatically strengthens the company’s book value and equity base. On April 8, TPIA shares were pressured by the general market rout, potentially ignoring this step-change in asset value. The “Consortium Defense” here is less about a formal buyback and more about the strategic accumulation of assets that act as a floor for valuation. The group’s infrastructure arm, Chandra Daya Investasi (CDI), which was listed in mid-2024, also provides a stable recurring revenue stream that reduces the overall beta of the TPIA holding structure.

The consortium’s strategy with TPIA has been to aggressively defend its market capitalization to support future fundraising for its world-scale CAP2 expansion project. A collapse in share price would increase the cost of equity and complicate debt financing. Therefore, the controlling shareholders have a vested interest in preventing the stock from languishing at distressed levels. The dip on April 8, driven by tariff fears that have only an indirect impact on domestic petrochemical spreads, allows investors to enter a company that has just booked a US$1.6 billion equity gain at a valuation that likely ascribes zero value to that transaction. The risk here is the inherent cyclicality of petrochemical margins, but the infrastructure pivot provides a growing cushion against that volatility.

Sector Analysis: Banking and The State Consortium (Himbara)

While the private conglomerates rely on internal treasury funds, the state-owned banking sector (Himbara) operates under a different form of consortium support—the implicit backing of the Republic of Indonesia and the explicit dividend mandates of the Ministry of State-Owned Enterprises (BUMN). The April 8 crash saw the banking sector decimated, with BBRI falling 7.65%, BMRI falling 8.27%, BBNI falling 4.48%, and BBTN falling 7.34%. This sell-off was driven almost entirely by foreign capital outflows, as these stocks are the most liquid proxies for “Indonesia Risk.”

However, the fundamental thesis for the banks remains intact. The transmission of a 32% US tariff to the Indonesian banking sector is weak. Domestic credit growth is driven by consumption and SME lending (in BBRI’s case), not export manufacturing. While a tariff-induced GDP slowdown of 0.5% would marginally impact loan growth, it does not justify a ~8% valuation haircut in a single day. The “Consortium Defense” for the banks manifests in their dividend yield. As prices fall, dividend yields rise, eventually reaching a level where domestic pension funds (Taspen, BPJS Ketenagakerjaan) are mathematically compelled to step in and buy to meet their actuarial return targets.

Furthermore, BBRI has a history of conducting share buybacks when its Price-to-Book Value (PBV) falls to attractive levels. With the April 8 plunge pushing valuations down, the probability of a state-sanctioned buyback or merely the accumulation by state-linked funds increases. The Himbara banks are the engines of the national economy; the government cannot afford for their equity values to collapse, as this would impact the capital adequacy ratios and the dividend revenue stream that supports the state budget. Therefore, buying the dip in BBRI and BMRI is a play on the “State Consortium” stepping in to stabilize its primary revenue generators.

| Ticker | Conglomerate / Group | Primary Business | Tariff Risk Exposure | Consortium Defense Mechanism | Status on April 8 |

|---|---|---|---|---|---|

| BREN | Barito Pacific (Prajogo Pangestu) | Geothermal & Wind Energy | Low (Domestic Contracted) | Official Share Buyback (IDR 2T) | Active Program (Mar-Jun 2025) |

| TPIA | Barito Pacific (Prajogo Pangestu) | Petrochemicals & Infra | Medium (Cyclical Spreads) | Asset Injection (Aster Acquisition) | Strong Balance Sheet Support |

| BBRI | BUMN (State-Owned) | Micro-Finance & Banking | Low (Domestic Credit) | Dividend Yield & State Support | Yield Support Zone |

| BMRI | BUMN (State-Owned) | Corporate Banking | Medium (Corp Loan Quality) | Dividend Yield & State Support | Oversold by Foreign Flow |

| ASII | Astra International (Jardine) | Auto, Mining, Palm Oil | Medium (IDR Weakness) | Strong Net Cash Position | Valuation Support |

Macroeconomic Context: The Currency and Policy Response

The April 8 equity plunge cannot be viewed in isolation from the currency markets. The tariff announcement triggered immediate pressure on the Rupiah, forcing Bank Indonesia (BI) to intervene in the offshore Non-Deliverable Forwards (NDF) market to stabilize the exchange rate. A rapidly depreciating Rupiah is a double-edged sword for conglomerates. For those with USD revenue (like BREN and TPIA’s export wing), it is a net positive. For those with USD cost bases and IDR revenue (like Astra’s auto division or consumer goods companies importing raw materials), it is a margin compressor.

The government’s response to the tariff threat is also a critical variable. Coordinating Minister Airlangga Hartarto’s mission to Washington is expected to yield a negotiated outcome. Indonesia has proposed purchasing US$15.5 billion in US energy and agricultural products and investing in US projects through the Sovereign Wealth Fund (Danantara). If successful, these negotiations could lead to the cancellation or significant reduction of the 32% tariff. Such an outcome would trigger a massive relief rally, particularly in the stocks that were punished most severely on April 8. Therefore, the “dip buying” strategy is also a geopolitical arbitrage play: betting that the transactionalist nature of the Trump administration will lead to a deal rather than a trade war. The “Consortium” stocks offer the safest vehicle for this bet because their internal defenses protect against the downside risk if negotiations drag on, while their beta allows them to participate in the upside if a deal is struck.

Strategic Recommendations and Forward Outlook

The April 8, 2025, market dislocation serves as a definitive stress test for the Indonesian equity market, revealing structural vulnerabilities in liquidity depth while simultaneously illuminating the resilience of conglomerate capital structures. For the institutional investor, the strategy is clear: bypass the broad market indices and focus capital allocation strictly on entities with active defense mechanisms. The “Buy the Dip” opportunity is not a blanket recommendation for the IHSG, but a targeted call on the “Consortium Put.”

Actionable Strategy:

- Prioritize BREN: The IDR 2 trillion buyback provides the most tangible floor. The 100% domestic revenue stream insulates against the tariff narrative. Accumulate on weakness, using the buyback execution period (through June) as the window of opportunity.

- Accumulate TPIA: The discrepancy between the $1.6 billion Q1 accounting gain and the depressed share price offers deep value. The infrastructure pivot reduces long-term volatility.

- Tactical Allocation to BBRI/BMRI: Use the foreign selling climax to build positions in the state banks. The dividend yield acts as a natural hedge, and the state backing ensures long-term solvency.

- Monitor Trade Talks: The catalyst for the next leg up (or down) will be headlines from the Airlangga-USTR meetings. A “deal” announcement is the trigger to increase beta exposure.

The risks remain elevated. A failure in negotiations or a disorderly depreciation of the Rupiah beyond 17,000/USD would challenge even the strongest consortium defenses. However, buying assets at -8% discounts in a single day, backed by billions in cash and state support, represents a skew of risk-reward that heavily favors the bold. The April 8 plunge was a liquidity event, not a solvency event. In the gap between price and value, the consortiums are buying. The astute investor should follow suit.

Disclaimer

aluna Analytics is an independent research collective that operates without affiliation to any financial institution, broker, or advisory firm. We do not hold licenses as a securities dealer, investment advisor, or portfolio manager.

All materials published by aluna Analytics are created solely for informational and educational purposes. They reflect independent analytical interpretation and should not be regarded as personalized investment advice, solicitation, or endorsement of any security or strategy.

Market data, opinions, and projections presented herein are subject to change and may not predict future results. Readers remain fully responsible for any financial decisions made based on the information provided. We strongly encourage conducting personal due diligence and consulting a licensed professional before making investment commitments.

aluna Analytics is not regulated by the Financial Services Authority of Indonesia (OJK) and does not offer investment management or brokerage services. All content is presented in good faith, aiming to foster research literacy and informed market perspectives.